UnderSpot Special Report: The Quiet Melting of Pre-’33 Gold

Date: January 9, 2026

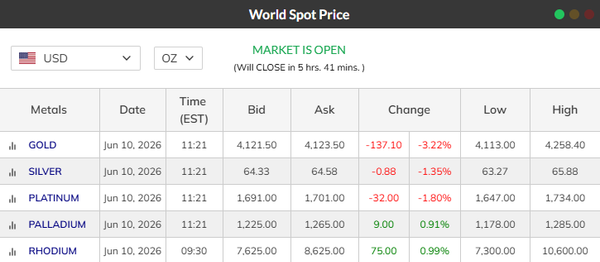

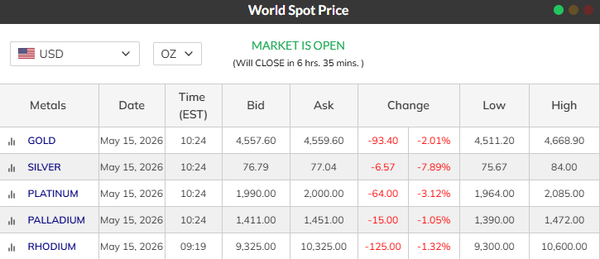

Spot Reference: Gold ~$4,500

Executive Summary

Pre-1933 U.S. gold coins are undergoing a quiet but meaningful shift.

Despite gold trading near historic highs, generic Pre-’33 gold is increasingly clearing in wholesale markets at or very near melt value, with traditional premiums either compressed, conditional, or absent altogether. This is not a retail illusion and not a temporary misprint, it reflects a liquidity-driven repricing in which ounces matter more than history.

Importantly, this shift does not mean Pre-’33 gold has lost relevance. It means the market has begun sorting coins from ounces, and not all Pre-’33 material is being treated equally.

Melt as the Anchor

In the current environment, melt value has reasserted itself as the dominant pricing anchor for generic Pre-’33 gold.

At current spot levels (~$4,500 gold), approximate melt values place:

- $20 gold coins just under mid-$4,300s

- $10 gold coins just over low-$2,100s

- $5 gold coins just over $1,080

These values are no longer theoretical “backstops.” In many cases, they represent real, executable exit points.

What Wholesale Pricing Is Signaling

Across multiple independent trading desks, the message is consistent:

- Common-date $20 gold coins are frequently bid at or within a narrow band of melt

- Any remaining premium is often:

- Grade-dependent

- Certification-dependent

- Thin and inconsistent

- Raw, generic material increasingly trades as metal with friction, not as a collectible

This does not indicate panic. It indicates prioritization of liquidity.

When ounces are scarce, capital expensive, and settlement timelines matter, markets default to what can be moved quickly and replaced easily.

Where Premiums Still Exist

Premiums have not vanished, they have become selective.

They persist in:

- Clearly higher-grade certified material

- Coins that are unambiguously numismatic, not interchangeable

- Pieces with immediate resale velocity and visual appeal

They have faded in:

- Generic common-date material

- Coins historically sold on the idea of Pre-’33 rather than demand

- Pieces that trade primarily on weight with a story attached

The market is not rejecting Pre-’33 gold. It is rejecting undifferentiated Pre-’33 gold.

What This Means for Dealers

For dealers, generic Pre-’33 gold has shifted from “heritage inventory” to working metal.

- Capital tied up in these coins earns little to no premium carry

- Bid-ask spreads increasingly resemble bullion spreads

- Exit strategies now assume melt optionality, not collector demand

In short: if it cannot trade as a coin, it must trade as gold….cleanly.

What This Means for Holders

For holders, especially those who accumulated Pre-’33 under the assumption of persistent premiums, this environment is clarifying.

- Liquidity now matters more than legacy narratives

- Premium recovery is no longer guaranteed, even at high spot

- The distinction between a collectible and a melt candidate is narrower than many expect

This is not a condemnation of Pre-’33 gold, it is a reminder that not all Pre-’33 gold is the same asset.

A Critical Counterpoint: Why Pre-’33 Still Makes Sense for Some Buyers

While wholesale premiums have compressed, Pre-’33 gold remains an attractive option for smaller buyers looking to add gold exposure.

For those purchasing:

- A few ounces at a time

- Fractional exposure via $5s or $10s

- Physical gold with historical character

Pre-’33 coins can offer:

- Competitive entry pricing relative to modern bullion

- Smaller denomination flexibility

- A tangible, recognizable form of gold ownership

At or near melt, Pre-’33 gold becomes a way to own gold with optionality, metal first, history included.

Why This Matters Now

Markets do not casually abandon premiums.

When coins that once carried unquestioned historical value begin trading as ounces, it signals a deeper shift toward liquidity preference and capital discipline.

This is not a headline event. It is a cycle signal.

And like most meaningful signals, it’s happening quietly…..right under spot.