UnderSpot: February 18, 2026

Backlog Clearing. Premiums Rebuilding.

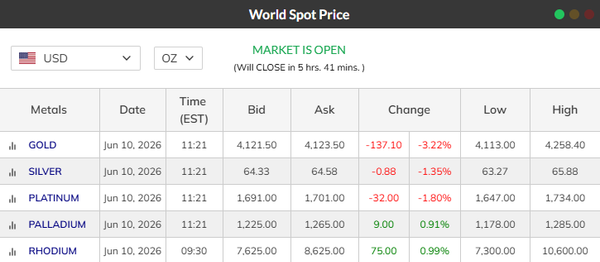

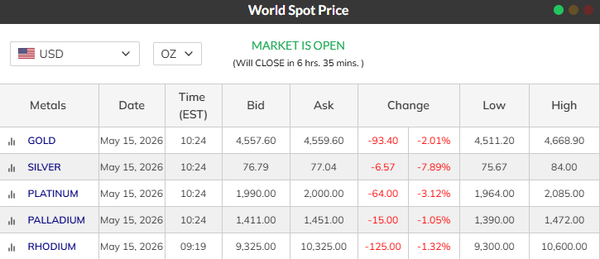

Spot at time of writing:

Gold: $5,004

Silver: $78.19

Platinum: $2,113

After weeks of extended delays and supply congestion, the physical market is beginning to change character.

Two national distributor sheets now show delivery windows measured in days instead of weeks for many core products. That alone is significant. The heavy backlog we’ve been tracking appears to be easing.

But the tightening hasn’t disappeared…. it has shifted.

Gold

Gold Eagles continue to hold firm.

Across national pricing this morning:

- 1 oz Eagles asking roughly 2.25% to 3.50%

- Fractionals ranging from roughly 5% to 8%

- Some 1/4 oz and 1/2 oz Eagles still showing multi-week delays

Premiums are not collapsing. They are rebuilding.

Even as spot pulls back slightly from recent highs, Eagles remain structurally expensive. Replacement is not effortless, and fractionals remain especially strong.

This does not feel like panic buying.

It feels like steady demand.

Silver

Silver remains a split market.

- 90% junk silver is being purchased again, though still at deep discounts.

- Generic rounds and bars are trading modest positive premiums on the ask side.

- 100 oz bars are being quoted consistently again.

- Some common silver products still show multi-week delays, but others are back to short-term fulfillment.

The most noticeable shift is in Silver Eagles.

- Current-year Eagles are firmly in the $10+ premium range

- Any-date Eagles are not far behind

That is a meaningful move from where we were.

Silver premiums are not euphoric, but they are no longer suppressed. The market is breathing again.

Platinum

Platinum remains tight and inconsistent.

Availability varies by distributor, and premiums remain clearly positive. Some products still show extended delivery windows, while others are beginning to normalize.

Platinum continues to behave structurally tighter than silver and more quietly than gold.

What This Means

The worst of the backlog appears to be clearing.

Metal is moving.

Settlement windows are shortening.

Premiums are firming.

The most interesting detail today is this: the distributor that previously discouraged selling with far-back bids and extended settlement times remains thinner than others. That tells you inventory rebuilding is uneven.

This isn’t a loose market.

It’s a market normalizing after strain.

And normalization, when paired with firming premiums, is not weakness.

UnderSpot Take

The congestion is easing, but the supply is not abundant.

Premiums are rebuilding quietly, and that matters.